Mon - Fri: 9:00 - 17:00

Sat-Sun Closed

Broad & Mechlin Street

info@mfdp.gov.lr

This brief has been necessitated by a misleading article authored by the former Minister of Finance and Development Planning, Mr. Boima Kamara, profiling Liberia’s debt situation and comparing debt performance before and after 2018. Mr. Kamara’s conclusions are fatally flawed and as a former minister, he was offered the opportunity to revise those conclusions to avoid the MFDP issuing a clarification, on the fact that he either may not have had the information that led to the faulty conclusions or did not discern the anomaly in the debt data. Mr. Kamara turned down the opportunity and asked the MFDP to issue the clarification.

Mr. Kamara’s conclusion reads thus:

In conclusion, the data shows a remarkably high rate of growth in public debt within 2 years 3 months of the current administration, compared with post-HIPC 7 years of the Sirleaf administration that ended in 2017. Fiscal dominance is slowly creeping given the borrowing pressure on the CBL, which runs contrary to the spirit of fiscal-monetary complementarity. In this regard, we advocate for greater support for the independence of the CBL as the monetary authority. At end-June 2020, the IMF and World Bank jointly classified Liberia’s risk of debt distress as MODERATE, something to claim the attention of policymakers. The debt-to-GDP ratio for Liberia has risen from around 30 percent during the Sirleaf Administration to 51.33[1] percent at end-March 2020. The journey of life after the debt is calling for appropriate fiscal rules and tougher vetting of future debt, which should be mainly for growth-enhancing projects with high economic returns and not for CONSUMPTION. As the budget hearing process starts, we call on the legislature to consider the facts above during the deliberations surrounding the proposed FY20/21 budget".

The above conclusion is correct in only one respect: that the stock of debt has grown over time and over the two periods under consideration in Mr. Kamara’s article. But Mr. Kamara failed to understand or investigate the reasons for the abnormal growth in the stock, an outcome that leaves his article seriously wanting. This reason should be apparent to any casual observer since the domestic debt stock cannot reasonably grow from US$264 million to $604.4 million in merely two years, a difference of $340.4 million, implying that the current administration borrowed on average $170.2 million in each of the last two years. With gross international reserves around $160 million at the end of 2017, the Central Bank of Liberia could never lend $170.2 million to the Government of Liberia yearly. Neither could the Government consume $170.2 million in goods and services in one fiscal year for which it would owe domestic vendors that amount. These facts and issues should have come out clearly to anyone investigating the debt numbers, compelling due caution and care in reaching conclusions.

There are two reasons why the debt stock grew between 2018 and 2020. The first reason is that disbursements on external loans from the World Bank, the African Development Bank, and other multilateral and bilateral creditors, signed by the previous administration, are happening now. When a loan is taken, the loan amount is recorded as borrowing but is not included in the official debt stock until the amount is disbursed or spent on the projects for which the loan was taken. For example, if the National Legislature ratifies a US$50 million loan and $10 million of this is spent six months after ratification, the debt stock, recorded and managed by the Debt Management Unit at MFDP, goes up by $10 million. The remaining $40 million is recorded as undisbursed and if canceled will be considered as borrowing.

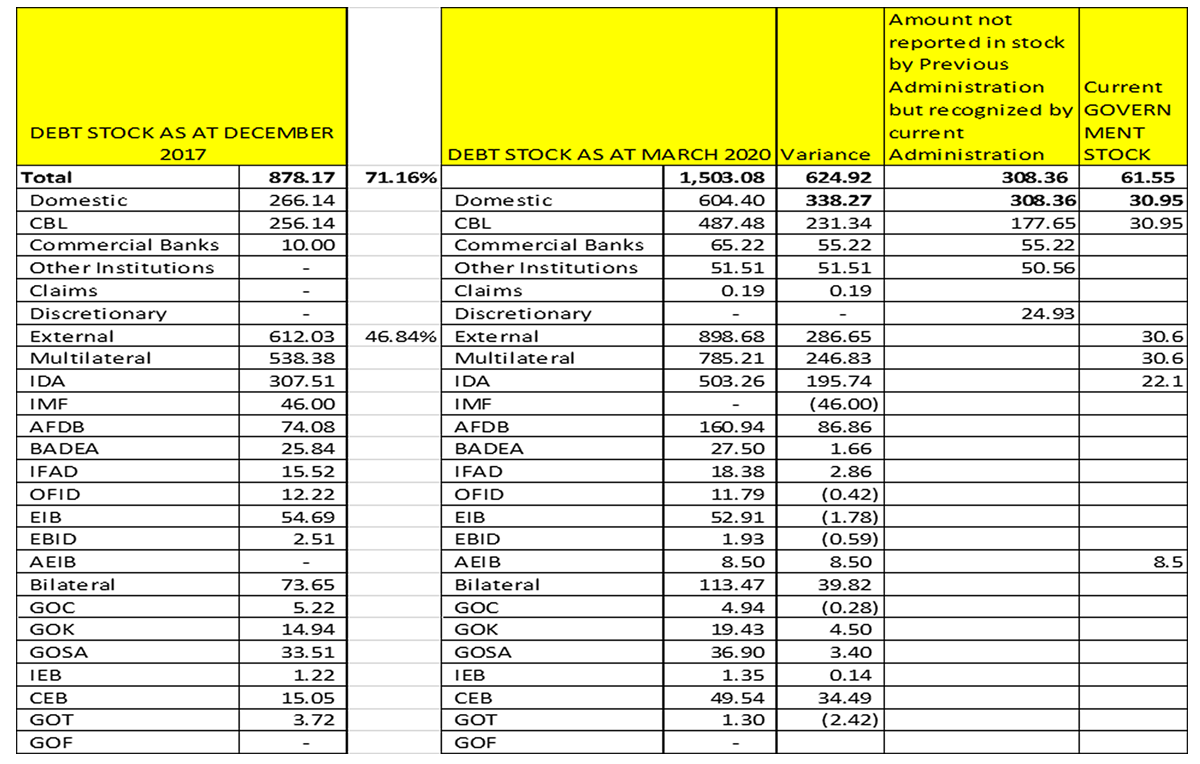

As of December 31, 2017, the total external debt stock was US$612.03 million. As of March 2020, total external debt stock stands at US$898.6 million. This means, US$286.65 million has added to the external debt stock since President George Weah took office. Of this US$286.65 million, US$256.05 million was added to the stock from borrowing/loans taken by the previous administration. The current administration is responsible for only US$30.6 million of the increase in external debt stock since 2018.

The second reason why the total debt stock went up has to do with accounting reconciliation of Government debt to the Central Bank of Liberia. This increase was paper or accounting money added to the domestic debt stock. These were monies that the previous administration did not recognize in the total debt owed to CBL. Prior to entry into the IMF program, the IMF insisted that the Government cannot continue carrying these unreconciled amounts in perpetuity but needed to validate and accept the debt as official Government borrowing from the CBL over the last decade or so. The MFDP had issues with bringing all these amounts as debt to CBL without a full audit. Some audits had been done by KPMG but MFDP folks still had issues with accepting the numbers. As such a lengthy negotiation between MFDP, CBL and IMF ensued and an understanding was reached.

Prior to these discussions, the total debt owed the CBL stood at US$256.14 million. After the reconciliation and negotiation, the new debt number was put at US$487 million, adding $202.58 million to the stock of debt owed the CBL by past Administration! This is what former Minister Kamara considers borrowing by the current administration. More to the point, the recognized debt should have been higher than $487 million, but the MFDP rejected some US$ 75 million which might be the subject of future audits though it is not in the recognized statistics between the Government of Liberia and the IMF.

Also, this paper addition of $202.58 million to the domestic debt stock is borrowing by the previous administration. If the previous administration had done the reconciliation and recognition carried out by the current administration, the total debt owed to CBL in 2017 would have stood at $456.53 million. With this, Mr. Kamara would not have written about an INCREASE IN DOMESTIC DEBT but probably about a decrease or stability under the current administration, since it is the new administration that is implementing a NO-BORROWING-FROM-CBL policy mandated by President George Manneh Weah.

The total amount borrowed from the CBL over the last two and a half years by the current administration is US$30.9 million. This is about 6.3 percent of the $487 million the Government of Liberia owes the CBL and this is most likely the only amount that would be borrowed by this administration under the no borrowing policy.

The other reason why the domestic debt went up is that the present administration recognized domestic debts to vendors and commercial banks in the tune of US$105.78 million that the previous administration did not recognize. This recognition deserves praise from former officials of the previous administration, rather than blame for ‘increasing the debt’. How does recognizing a legitimate debt from the past become ‘borrowing’ under the new administration? The Government issued a US$65 million bond to commercial banks, bringing value to the books of these banks. Many were on the verge of writing the loans off because they thought the Government would never pay. These bonds are today among the most valuable assets owned by the banks.

The new administration did the same thing for US$50 million the Government owes the National Social Security and Welfare Corporation (NASSCORP). In fact, negotiation of this very bond started under the former minister Boima Kamara but was finalized by Minister Samuel D. Tweah, Jr. How and why these bonds are seen by the former minister as a problem as opposed to a solution is really not clear.

The below table from the Debt Management Unit at MFDP summarizes the arguments made above and is a useful guide for the public and investigators to understand the evolution of the stock of debt and the factors behind the movement. Such a period by the period breakdown of debt statistics might now be made an official part of the debt report considering the unhealthy appetite of many political actors to exploit and distort Government data for political purposes.

Conclusion

It is clear from the above the conclusion reached by the former Minister is uninformed and unwarranted. The current Government’s contribution to the total stock of RECOGNIZED and VALIDATED debt is about $61.5 million, 30.6 million from external borrowing, and 30.9 million from the CBL. This does not include debt owed to vendors who have supplied goods and services over the years. As with other debt statistics, the Government is undertaking a reconciliation and validation of these numbers to include in the official debt statistics. This is why debt owed to vendors are not shown in the above table. Once this recognition is done, of course, the domestic debt numbers will increase. These figures span the last 12 to 14 years.

The former minister’s conclusion on fiscal dominance is also unwarranted. Under the fiscal and monetary reforms the Government has carried out, fiscal dominance is a thing of the past. The no-borrowing-from-CBL policy is the strongest indication of the end of monetary accommodation or fiscal dominance. The CBL now has an interest-rate based monetary policy framework, while the MFDP has a new liquidity management framework that prevents the accumulation of arrears. The MFDP passed three out of four quantitative performance criteria (QPC) under the current IMF program, and one of them would of course be the on QPC on the primary deficit since the fiscal has now achieved a budget surplus in the last fiscal year.

The former Minster’s other concern about debt to GDP ratio is also misguided. The key statistics we now look at is debt service to GDP ratio. And even if we were merely to look at debt to GDP, this ratio cannot be put on the current administration, Liberia’s debt to GDP is among the lowest in the region. Our current IMF program is designed to ensure we create maximum space to service debt largely inherited from the previous administration. Our borrowing space is severely limited and with COVID and economic shocks, we may face challenges, forcing us to tighten fiscal policy to save resources and limit Government borrowing.

Mr. Kamara’s concerns about debt sustainability are well placed and both the MFDP and the Government share these concerns and are taking steps to prevent a debt crisis. We have launched a new debt sustainability review process, are validating the stock of domestic debt, and have placed $10 million in the FY 2021 budget to service domestic arrears.

It is quite unfortunate that the former Minister has reached these unwarranted and assailable conclusions when a simple inquiry into the factors underpinning the debt numbers could have avoided a situation where his false conclusions would provide fodder to politicians and political pundits gunning for the reputation of the current administration.

P. O. Box 10 - 9016

Broad & Mechlin Street

1000 Monrovia

info@mfdp.gov.lr